Debt and depression can often go hand in hand.

While her student debt topped out at $81,000, Melanie Lockert was earning just $10-12 an hour living in New York City. She felt trapped, unable to move forward and make financial progress. She started a blog Dear Debt to write about her experience.

“Debt is paying for your past, not paying for your present or your future,” Lockert says. For her and many people, she says, that feeling of helplessness and despair around debt can lead to depression.

The Links Between Debt and Depression

If you’re struggling with debt and depression, you’re not alone. Nearly half (45%) of Americans have felt depressed about their financial situation lately, according to a Student Loan Hero survey. And student loan borrowers were twice as likely to feel depressed about their finances.

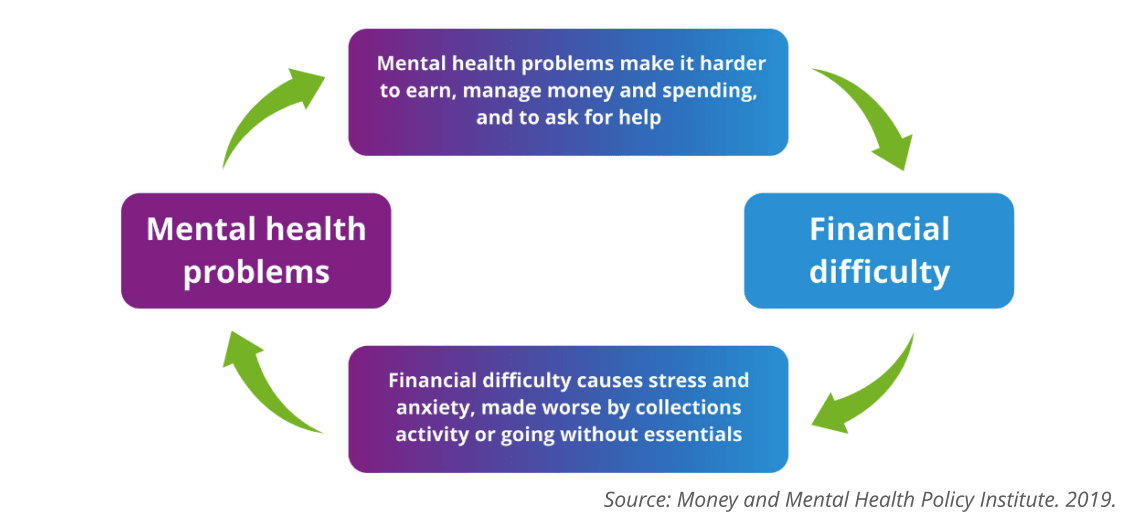

Experiencing money and mental health problems at the same time can even create a cycle with each problem feeding into the other, as illustrated by the Money and Mental Health Policy Institute in England.

Financial stress and difficulties can contribute to mental health problems, which in turn make it harder to manage money and seek appropriate support.

On top of this, debt and money are still considered taboo topics of discussion — making it harder to get social support. This can contribute to feelings of isolation and shame about debt. And the costs of debt can make it difficult to afford, access, and pay for professional help and support, such as therapy or mental health treatment.

Pre-existing depression or mental health problems can also make it difficult to manage money and even result in further debt, says Katherine Iesiev, LICSW, CFSW, founder of She Minds Money, a financial therapy and coaching service for women. Depression or mental health concerns can affect finances “through unstable employment, reduced financial coping skills, or increased spending on convenience when energy and motivation are low,” Iesiev says.

Manage Depression and Mental Health First

If you’re experiencing depression that’s related to your debt, you’re not alone.

“Your mental health comes first,” Iesiev says. “Without taking action to alleviate your depression, it will be that much more difficult to make progress on your debt.”

If you are having thoughts of suicide, seek immediate help through local behavioral crisis center, the emergency room, or a national suicide hotline, Iesiev urges. Call the national hotline at 800-273-8255, or visit SuicidePreventionLifeline.com.

Additionally, “When depressive symptoms last for more than two weeks or start to interfere with your functioning in your family, at work, or at school, then it’s a good time to seek [professional] help,” she says.

Beyond seeking professional help, here are some ways to support your mental health and manage depression.

Separate yourself from your debt. “Try to uncouple your self-worth from your net worth, or the size of your debt,” Iesiev says. Recognize that your debt is just a number and doesn’t define you or your life. You deserve to feel better and minimize stress, regardless of debt.

Explore mental health supports and solutions. Brainstorm ways you can support your mental health, such as getting more sleep or taking time off of work.

Make a list of options to explore such as seeing a financial therapist, seeing your doctor for medication, or developing mindfulness or stress management skills, Iesiev advises.

Here’s more information about financial therapists.

Seek help from others. Talk to a trusted friend, family member, spiritual leader, or therapist about what you’re going through. You can also ask for support, whether that’s ongoing check-ins or help with specific tasks like finding a therapist.

Start small, but focus on impact. You can’t try every option or potential solution at once, and that’s okay. Even small steps in a healthier direction can put you on the path to effective depression management and relief.

Identify an action that feels more doable, or will have the biggest positive impact (ideally, both) and make a plan to take it.

Manage Your Debt and Chart a Path Forward

When facing debt and depression, financial strategies can also be a lifeline. Managing debt more effectively can ease financial pressures and stress, and help you create a path forward.

“The process of debt repayment actually provides some good opportunities for building self-esteem and confidence in your abilities — which can be protective for mental health,” Iesiev says.

First, face the numbers. Start small: look up and record the balance, payment, due dates, and interest rate for one or two accounts until you have all your debts recorded. Next, collect other information like your income and other expenses.

Triage your debt. If you have delinquencies or past due balances, work to get current on those accounts first. Reach out to your lenders and see if they can offer a hardship deferment or lowered payments. If your debt would take five or more years to repay, consider bankruptcy and other options.

Make a debt payoff plan. Making extra payments on debt will help you eliminate it faster. Compare strategies like the debt snowball or the debt avalanche method, Iesiev suggests, and choose the debt repayment plan that makes sense to you. Play with debt pay-off calculators can help you see what’s possible, and how much time and money different strategies could save you.

Set smaller goals within your plan. For example: making on-time payments for six months, paying off your first $1,000, or paying an extra $180 each month. Then track your progress, Iesiev suggests, using debt charts to keep progress visible. Finally, celebrate progress along the way and reward yourself when you hit smaller goals, maybe by ordering out or even just sharing your win with a friend.

Balance debt repayment with quality of life. Lockert aggressively repaid her student debt in 5 years, but “there are some things I regret, and I became unhealthily obsessed,” she says. Don’t let debt repayment become your whole life. Avoid overworking to earn extra money to the point of burnout, she advises. And leave room in your budget and schedule for those things that make life worth living.

Managing debt and depression may not be an easy, fast, or simple process. Depression makes it hard to believe it’s possible for things to get better.

But it is possible. You can get the support you need. You can find mental health tools that lift some of the weight, and financial strategies that work for you. Start with just one of the suggestions here, then another. You can build a path forward to a future where debt and depression no longer hold you back.

0 Comments