Debt is an ugly word.

I feel uneasy every time I hear or look at it but that could also be because of my bias towards it.

Having watched debt take away joy, time, and almost entire lives from people, I can’t help but be triggered by the word.

According to Bankrate, consumer debt in America is $14.2 trillion dollars with an average personal debt of $92,727 in 2021.

But it is nothing you should be ashamed about.

Where to Start

First, let’s get past the shame and fear you feel around your debt and money. Our relationship with money is almost always very personal and very emotional. Once we face those feelings head on, they no longer have power over us and we can go on living our lives without that weight.

Our debt isn’t something we should feel bad or beat ourselves up about. This will only dig us further into a hole

Instead, we must recognize that it happened but move on and start fixing it.

Before you decide on a debt paydown strategy, you first need to know how much debt you exactly have.

If you know what accounts you need to log in to, to get this information, you’re in a great spot.

Log in to each account and write down in a spreadsheet each of the following:

- The name of the loan

- What it was for

- The amount left to pay

- The interest rate

- If it is on any special repayment plan, currently deferred, or in forbearance

Let’s say you don’t know what debt you even have. Then I suggest you use something like AnnualCreditReport.com to pull for free all the current loans and lines of credit that are open.

5 Strategies to Get Out of Debt

You’ll likely want to choose either the snowball method or the debt avalanche to choose the order in which you will pay off your debts. Then, really, the plan is to throw as much money as possible at your debts until they are gone.

1. Use The Debt Avalanche Method

The Debt Avalanche method is an accelerated debt repayment method that works best for folks with high-interest debt and many sources of debt. The idea behind it is you pay off high-interest rate debts first so, in theory, you are paying the least amount of money possible in your debt repayment plan because you avoid having the highest interest rate debt accumulate any further.

How it works is you allocate enough for just the minimum payments on lower interest rate loans and then allocate the remaining of the repayment funds to the loan with the highest interest rate. Once that one is paid off, then your highest allocation goes to the next highest interest rate. Then that process repeats until all debt is paid off.

2. Use The Debt Snowball Method

The Debt Snowball method is a debt repayment strategy where you pay off your debt in order from smallest to largest.

So, if your lowest remaining amount on a loan is $3,000 and your highest is $30,000, you start paying the most on the $3,000 loan and the minimum payments on all other loans. Then you repeat the process and move on to the next highest loan until all debt is repaid.

3. Pay More Than The Monthly Minimum Payment

Paying the minimum payment will only prolong the debt and because of interest, you will end up paying much more over time.

If you don’t already keep a monthly budget and track your spending, you will need to do so to see how much extra you can start paying down towards debt monthly.

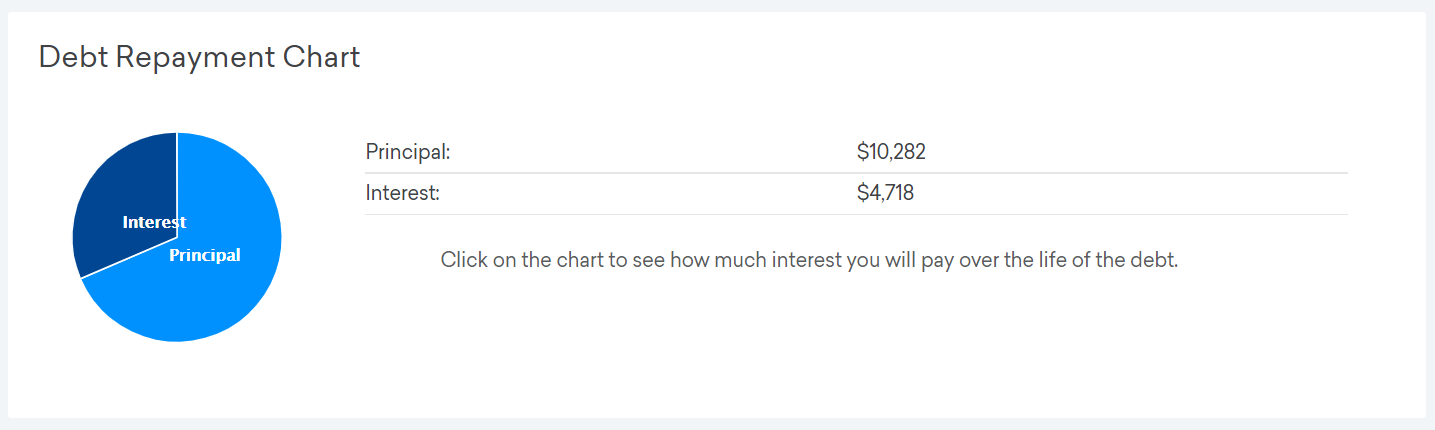

This is especially important for credit card debt that has the highest interest rate of all. If you paid the minimum payment on a $10,000 credit card bill of $300 at 20% APR, you will pay $4,718 in just interest over the 50 months it would take to pay that bill off (assuming you don’t take on more credit card debt during that time).

Image credit: Credit Karma

A great way to decide how much extra you want to start paying every month and how long it will take you to pay it off is by using a debt repayment calculator like the one at Credit Karma or implement the same formulas into your spreadsheet.

4. Refinance Your Debt

Let’s say you want to start reducing the interest you pay on your debt while you repay it, then you can look into refinancing that debt to a lower interest rate.

You can do this by contacting your loan servicer to refinance your auto or home loan but usually want to wait to do so until your credit score improves, loan rates go down, and you have positive equity or through a consolidation loan.

If you have a lot of credit card debt, you can do this by transferring the debt to a balance transfer card with 0% APR for a certain timeframe.

5. Commit Windfalls to Debt

When you get large sums of money from any of the following, you can transfer those funds directly towards repaying your debts:

- Tax refund

- Stimulus check

- From selling something of value

- Side hustle income

- Bonus checks from your employer

- If you get a raise at work – commit a percentage of it to your debt

- And any large sums of money

Look Into a Debt Settlement Service

If your debt has gotten out of control over the years and has risen to levels you don’t think you will ever be capable of paying off, you can look into a debt settlement service to help you settle for less than the amount of the loan.

You can contact third-party debt settlement companies to help you do this.

Join a Supportive Community

There is a growing online community that has formed out of the increasing number of people in debt and those same people trying to dig themselves out of it. It is called the Debt Free Community.

You can follow folks in this community using the #debtfreecommunity hashtag on Instagram and on reddit in the r/debtfree subreddit.

Conclusion: Your Debt Free Journey

When you are just starting your debt free journey, things can be very overwhelming. Try not to dwell on the numbers and the long road ahead.

Instead, I recommend using creative motivational methods like debt repayment color in charts to help you stay on track towards your goal.

Other ways to stay motivated towards the end goal are:

- Regularly track your debt repayments in a google spreadsheet

- Take yourself out on solo date to celebrate milestones (or do it with friends and family)

- Do a monthly debt recap of how much you started with and how much you have left after that month’s payments

This road can be a lonely one. Confide in a community to discuss pain points, what worked, what didn’t, and your goals. When you connect with others on the same path, it can work wonders for your own journey with those community resources.

You got this.

0 Comments