The argument that “anyone in America can build wealth” is flimsy financial advice. When added to “The only thing holding you back is you” and “If you’re just willing to work hard you can become a millionaire,” you get a set of outdated beliefs that ignore the role that racism played (and continues to play) in the creation of wealth in America.

Yes, anyone “can” build wealth in America, but quotes like this ignore the fact building wealth is much more difficult for certain groups. This difficulty level is often based on race and not work ethic. One of the main generators of wealth in the U.S. has been hundreds of years of laws and policies that have worked to advance one group of people, while actively working to ignore or exclude others. While some of these laws were enacted over 150 years ago, they still have a very significant impact today.

The Impact of the Homestead Act

In 1862 Congress passed the Homestead Act which distributed 246 million acres of land across the next 60 years to 1.5 million families. Today, that land would be worth between $740 billion to $1.6 trillion as of 2015. That is the equivalent of giving approximately $500,000 to $1 million per family. However, of those 1.5 million families that received homestead land, 99.73% went to white families. Researchers estimate that up to 93 million Americans today are direct beneficiaries of that program.

Today, the typical net worth of a white family in America is 10 times greater than that of a Black family. Between 1989 and 2013, the average 401(k) savings for white people was more than $130,000 compared to African-Americans at just $19,000 and Hispanic Americans at $12,000. This is known as the racial wealth gap, the difference in the median wealth between ethnic groups.

Other Practices that Encourage the Racial Wealth Gap

While the Homestead Act still benefits more than 90 million people today, there have been a series of laws since then that have helped to perpetuate the racial wealth gap.

In 1944, the federal government invested $95 billion via the GI Bill to create opportunities for returning soldiers. That is the equivalent of $700 billion today but, less than 2% of that money went to the 1.2 million Black veterans who served in World War II. This left Black veterans out of the post-war housing boom. In New York and northern New Jersey, less than 100 of the 67,000 mortgages insured by the GI Bill supported homes purchased by non-whites.

Even for Black homeowners who are able to secure funding, they still faced struggles. Researchers from George Washington University found that Black homeowners receive 18% less value for their homes than white homeowners at about $48,000 per home. On top of owning homes that are worth less, the Economic Policy Institute found that Black Americans with a 660 FICO credit score are three times more likely to receive higher interest rates then white Americans with a 660 credit score.

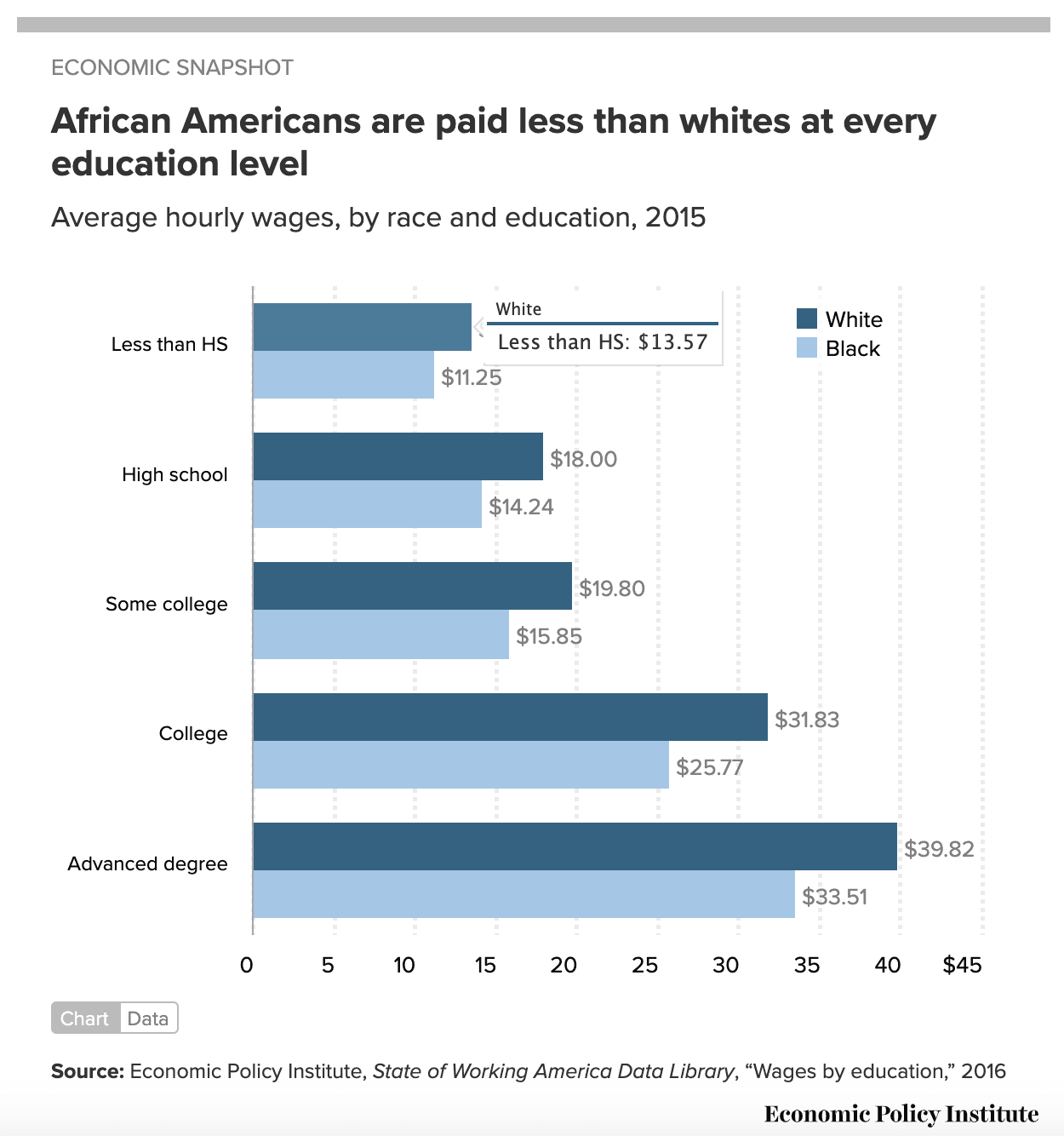

When we talk about “hard work” and “building wealth” this normally involves obtaining a college degree and/or a high-paying job but even these avenues of obtaining wealth are not equally beneficial. Data from 2016 indicates that Black college graduates have nearly $25,000 more in student loan debt at an average of $52,726, compared to $28,006 for the typical White bachelor’s graduate. Despite paying more for a college degree Black graduates still face an unemployment rate that is double the rate of their white peers. African Americans are also often paid less at every education level.

The Economic Policy Institute found that 85% of Black people need to have Bachelor degrees for Black Americans to have the same employment rate as white Americans who have a 36% rate of college degree attainment. Right now, Black bachelor’s degree holders are at just 24%.

These costs start to add up quickly if you’re not white: Higher unemployment rates, lower pay, higher costs for education, and lower returns on real estate all combine to make things considerably more difficult to build wealth. While these stats may not be uplifting there are at least some solutions that could help push things in the right direction.

Potential Solutions

Keep in mind that while individual decisions can be helpful in closing some aspects of the wealth gap, it was not individual choices that led to the problems stated above. In many cases, it was years of policies and discrimination at every level. Solutions to the wealth gap will take similar efforts to reverse the trends that we’ve seen over the last several decades. But as Courtney Richarson, founder of The Ivy Investor said, “It has to be macro and micro. Macro in terms of state and federal policies. Micro getting rid of money drains and providing good financial literacy.”

Below we will discuss potential solutions from both the policy level (macro) and the individual and community level (micro).

Policy Level

Baby Bonds

The concept of “Baby Bonds” also known as the American Opportunity Accounts Program gained traction with New Jersey Senator Cory Booker in 2018. Here’s how the program would have worked:

- Every child born would receive $1,000 to start.

- Through the tax code, kids would receive up to $2,400 depending on family income.

- The money would grow at 3% each year in a low-risk account managed by the U.S. Treasury.

- The money couldn’t be used until age 18. At that point, the money could be used only for education, homeownership, or retirement.

Based on how wealth is currently distributed, Black children would receive more than $29,000 and Latino families would receive more than $27,000 through this program at age 18, as compared to white children who would receive nearly $16,000.

Minimum Wage

Since 2009, the federal minimum wage has remained unchanged at $7.25 per hour (and $2.13 for tipped workers). In recent years there have been several successful campaigns that have fought for a $15 minimum wage. Among those are California, New York, Illinois, Connecticut, and Maryland — just to name a few.

Raising the minimum wage has been shown to:

- Increase worker productivity

- Reduce poverty and reliance on public assistance programs

- Improve infant health and adult mental health, including a significant reduction in depression according to the 2017 Road to Wealth study by Prosperity Now and the Institute for Policy Studies.

Encourage businesses to spend in Black and Brown communities

In the 1970s Atlanta Mayor Maynard Jackson mandated that 25% of construction contracts be set aside for businesses of color. According to the Greenlining Institute, that decision resulted in $1.6 billion being awarded to minority firms.

In a similar move, Netflix made headlines earlier this year by announcing a $100 million investment into Black organizations and Black banks. Encouraging all Fortune 500 companies to spend just 5% of their earnings with minority-owned businesses, banks and Historically Black Colleges and Universities (HBCUs) could create significant opportunities to close the wealth gap.

Individual and Community Level

Financial Literacy

In the past, I have argued that financial literacy is not “enough” to solve the problem of wealth and income inequality but, that if implemented correctly, there can be several positive results. One of the positive results could include avoiding the trap of payday loans which tend to prey on unbanked and underbanked communities. Each year on average, a borrower takes out eight loans of $375 and pays $520 in interest. A well-timed financial literacy program could help offset some of these common pitfalls.

Openly Discuss Your Finances

Communication about money is the biggest micro differentiator added, Richarson. Not only does this include wealth transfer tools like wills and life insurance but it can also include being transparent about your income at work.

Together these solutions can work to create greater access and opportunities. Access is critical, says, Holly D. Reid, CPA and financial educator, “Often it takes us twice as long to reach levels of success because we are so busy chartering the path without much help. Access provides the opportunity for us to shine.”

For more information on this subject, watch our webinar on the racial wealth gap, which includes Kevin L. Matthews II. You can also listen to our podcast episode about systemic money issues.

0 Comments